One year ago, the One Big Beautiful Bill Act created a new savings vehicle for children: the Trump Account. As of July 4, 2026, these accounts are open for contributions, and the IRS reported nearly six million elections to establish them even before contributions began. For parents and grandparents, the natural question is where this new account fits alongside the two vehicles families have relied on for decades, the 529 education plan and the UTMA custodial account.

Our view reflects an emerging consensus among planners: Trump Accounts are clearly worth opening, particularly for children eligible for the government’s $1,000 seed contribution, but they are a less compelling destination for a family’s own savings dollars. The reason comes down to how each account is taxed on the way out, not just on the way in. This paper walks through the mechanics of all three vehicles and offers a practical order of operations.

How Trump Accounts work

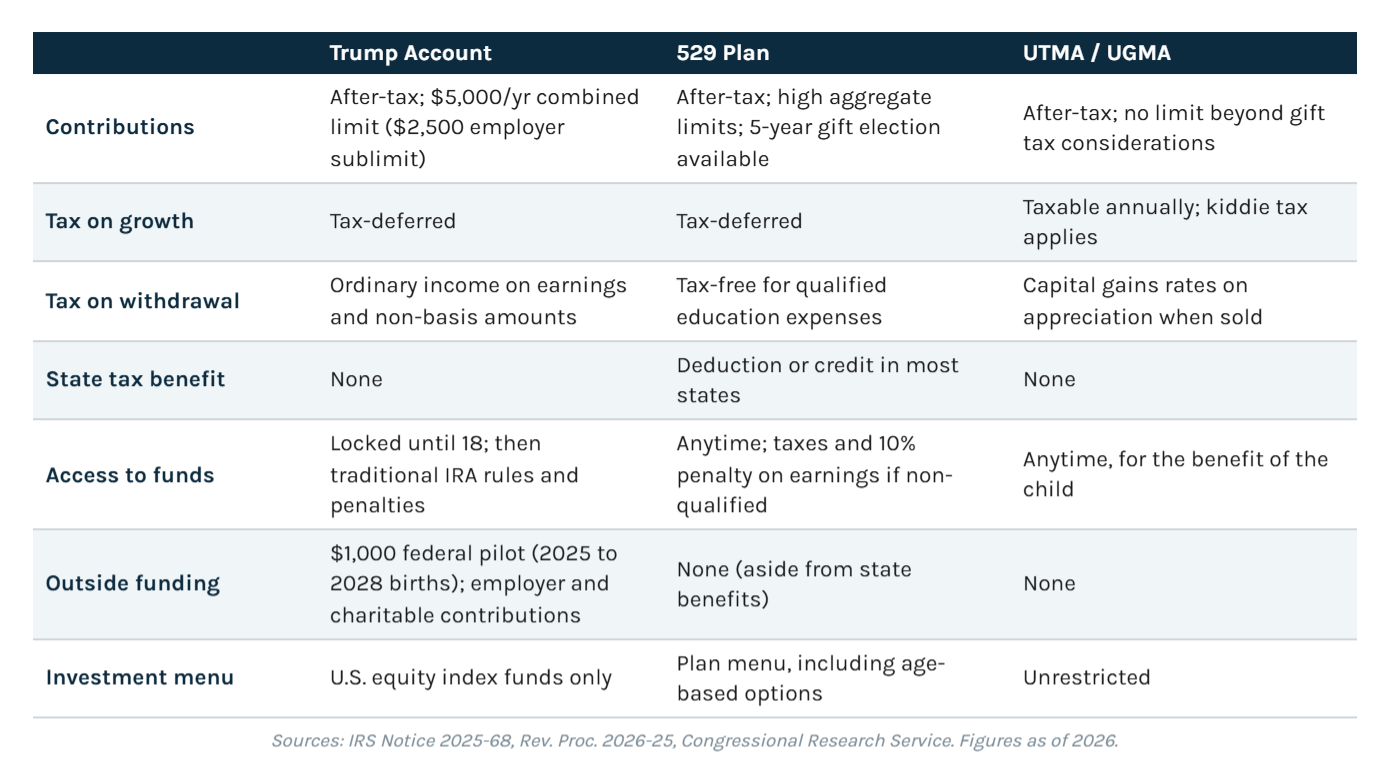

A Trump Account is a special form of traditional IRA that can be opened for any child under 18 with a Social Security number. Parents or guardians make the election through IRS Form 4547 or online, and accounts are initially administered by BNY. The account operates under distinct rules during its “growth period,” which runs from birth through December 31 of the year before the child turns 18.

Three features define the growth period. First, contributions from all individuals are capped at a combined $5,000 per year (indexed for inflation after 2027), and unlike other IRAs, the child needs no earned income. Employers may contribute up to $2,500 per year to an employee’s or dependent’s account, which counts against the $5,000 limit but is excluded from the employee’s taxable income. Contributions from governments and charities sit outside the limit entirely; the Michael & Susan Dell Foundation, for example, has pledged $250 contributions for millions of eligible children. Second, investments are restricted to low-cost mutual funds or ETFs tracking the S&P 500 or similar U.S. equity indexes. Third, the money is locked: with narrow exceptions, nothing can be withdrawn before January 1 of the year the child turns 18.

The headline benefit is the federal pilot program. Children born from 2025 through 2028 receive a one-time $1,000 deposit from the Treasury, provided a parent makes the election. Recent guidance has also removed a practical annoyance: under Revenue Procedure 2026-25, contributions generally will not trigger gift tax return filings so long as total annual gifts to the child stay within the $19,000 annual exclusion and a few other conditions are met.

Once the growth period ends, the account simply becomes a traditional IRA. It can be rolled to another custodian, converted to a Roth, or left to compound, and standard IRA distribution rules apply, including the 10% penalty on most withdrawals before age 59½, with familiar exceptions for higher education and a first home purchase.

The tax treatment is the catch

Here is where enthusiasm should be tempered. Individual contributions to a Trump Account are made with after-tax dollars and are not deductible. Yet withdrawals of earnings are taxed as ordinary income, just like any traditional IRA. In other words, the account combines the worst input (no deduction) with the worst output (ordinary income rates) among tax-advantaged vehicles. Families are effectively converting what would have been long-term capital gains and qualified dividends, taxed at 15% or 20% in a taxable account, into ordinary income taxed at rates as high as 37%.

The basis rules add another wrinkle. Only out-of-pocket contributions from individuals create basis. The government’s $1,000 pilot deposit, employer contributions, and charitable contributions carry no basis, meaning those dollars and all growth on them are fully taxable at withdrawal. Tax deferral over several decades has real value, and for a child with no other IRA the eventual Roth conversion math can be attractive. But deferral alone is a modest prize when the alternative vehicles below offer either fully tax-free withdrawals or preferential capital gains rates.

How 529 plans compare

For education savings, the 529 plan remains the gold standard, and nothing in the new law changes that. Earnings grow tax-deferred and come out entirely tax-free when used for qualified education expenses, a category that now spans college, graduate school, apprenticeships, expanded K-12 tuition allowances, and certain credentialing costs. Most states also offer a state income tax deduction or credit for 529 contributions, subject to state-specific limits and rules, an incentive with no parallel in the other two vehicles.

529s are also far more capable as wealth transfer tools. There is no $5,000 ceiling; a grandparent can front-load five years of annual exclusion gifts at once, up to $95,000 per beneficiary ($190,000 for a married couple) in 2026, removing those assets and their future growth from a taxable estate. And the old objection, “what if my child doesn’t need it for school,” has softened considerably: beneficiaries can be changed within the family, and up to $35,000 of long-held 529 assets can be rolled into the beneficiary’s Roth IRA over time, subject to annual IRA limits. For financial aid purposes, a parent-owned 529 is assessed as a parental asset, a more favorable treatment than a custodial account receives.

How UTMA accounts compare

The custodial UTMA account is the flexibility play. There are no contribution limits beyond gift tax considerations, no restrictions on investments, and broad latitude on use, so long as spending is for the child’s benefit. Funds can pay for a car, a wedding, or a first business, or simply transfer wealth. The trade-off is twofold: taxes along the way, and control at the end.

On taxes, custodial accounts generate annual taxable income subject to the kiddie tax. In 2026, the first $1,350 of a child’s unearned income is tax-free, the next $1,350 is taxed at the child’s rate, and anything above $2,700 is taxed at the parents’ marginal rate. That sounds punitive, but note what is being taxed: long-term gains and qualified dividends still receive preferential capital gains rates, just potentially at the parents’ bracket. A tax-efficient index portfolio inside a UTMA can defer most gains for years and ultimately pay 15% to 20% on appreciation. Compare that with a Trump Account, where, absent a later Roth conversion, growth eventually comes out at ordinary income rates. On control, UTMA assets belong irrevocably to the child and transfer outright at the age of majority, and custodial assets weigh more heavily against financial aid eligibility.

A side-by-side view

Open the account, think before funding it

Pulling this together, families may find a simple order of operations useful. First, claim the outside dollars. If your child or grandchild was born between 2025 and 2028, making the election to receive the $1,000 federal contribution costs nothing. If your employer offers Trump Account contributions, they are generally worth accepting, since $2,500 per year excluded from taxable income is a genuine benefit that has no equivalent in a 529 or UTMA.

Second, direct education savings to a 529. The combination of a potential state tax deduction going in, tax-free growth, tax-free qualified withdrawals coming out, and the Roth escape hatch is difficult to match for education goals. Third, use a UTMA or a parent-owned taxable account for flexible, non-education goals, where preferential capital gains treatment and full liquidity outweigh the modest annual kiddie tax drag. Only after these buckets are addressed should discretionary dollars flow to a Trump Account, and even then, the strongest case involves a plan: for instance, converting the account to a Roth IRA in the child’s low-income years after age 18. The conversion itself is taxable, but at a young adult’s low rates it can transform an ordinary-income liability into decades of tax-free compounding.

The bottom line? Trump Accounts are good to open and less attractive to fund. Claim the $1,000 pilot contribution and any employer dollars, then send your family’s own savings to a 529 for education and a custodial or taxable account for everything else, where the tax treatment on the way out is meaningfully better.

Disclosure: Stonebrook Private LLC (“Stonebrook”) is a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not constitute an endorsement of Stonebrook by the SEC nor does it indicate that Stonebrook has attained a particular level of skill or ability. This material is provided for educational and informational purposes only and does not constitute investment advice, a recommendation, an offer to buy or sell, or a solicitation of any security, strategy, or investment product. Saving for children involves legal and tax considerations; Stonebrook does not provide legal or tax advice, and you should consult qualified legal and tax professionals regarding your specific situation. Contribution limits, tax rates, exclusion amounts, and other figures reflect federal law and IRS guidance in effect as of the publication date and are subject to change; Trump Account rules in particular remain subject to modification as the Treasury Department and IRS issue final regulations. State income tax treatment of 529 plan contributions varies by state; deductions or credits may be limited or unavailable depending on the taxpayer’s state of residence and the plan selected, and some states offer benefits only for contributions to their own plans. Features of 529 plans, custodial accounts, and individual retirement accounts vary by state, plan, and custodian, and the treatment of these accounts for financial aid purposes is determined by program rules that may change. References to third-party organizations, programs, or account providers are for informational purposes only and do not constitute an endorsement or recommendation. All investing involves risk, including the possible loss of principal. Past performance is not indicative of, and is no guarantee of, future results. Information herein was obtained from various sources believed to be reliable; however, Stonebrook does not guarantee, and accepts no liability for, the accuracy or completeness of information provided by third parties. Sources include the IRS, U.S. Department of the Treasury, and Congressional Research Service.