Healthcare is often the single largest, and most unpredictable, expense retirees face. Over a typical 25- to 30-year retirement, cumulative out-of-pocket costs can easily reach several hundred thousand dollars. While coverage comes from many sources, Medicare sits at the center of the equation for most Americans age 65 and older.

Despite its importance, the program’s rules remain a source of confusion. Enrollment windows, income-based surcharges, and the choice between competing plan structures all carry financial consequences that extend well beyond monthly premiums. For families building a retirement income strategy, getting these decisions right can help protect savings, maximize coverage, and maintain cash-flow stability across decades of retirement.

Why Medicare matters today

Signed into law in 1965, Medicare originally consisted of Part A (Hospital Insurance) and Part B (Medical Insurance). Congress has since expanded the program to cover prescription drugs and additional benefits. Today, Medicare provides health coverage for more than 68 million Americans, including roughly 61 million people age 65 and older and 7 million younger individuals with qualifying disabilities.

The program’s significance has only grown alongside rising healthcare costs. In 2024, national health expenditures reached approximately $15,474 per person, accounting for about 18% of GDP, and spending is projected to outpace economic growth over the coming decade. For retirees, many of whom rely on fixed income streams, Medicare provides essential relief against those rising costs.

The program is structured into four parts, each serving a distinct role:

• Part A covers inpatient hospital stays, skilled nursing, and hospice care. It is typically premium-free for those who have worked at least ten years.

• Part B covers physician services, outpatient care, and preventive services. It requires a monthly premium that is subject to income-based surcharges.

• Part C, known as Medicare Advantage, is offered by private insurers as an alternative to Original Medicare. These plans often bundle dental, vision, and hearing coverage.

• Part D provides optional prescription drug coverage through private insurers and is also subject to income-based surcharges.

A common misconception is that Medicare is free because individuals have contributed through payroll deductions throughout their careers. While Part A is indeed covered for most people, Part B premiums, supplemental coverage, and out-of-pocket costs can add up significantly. That is precisely why integrating Medicare decisions into a comprehensive financial plan is so important.

The Medicare income cliff: why IRMAA planning matters

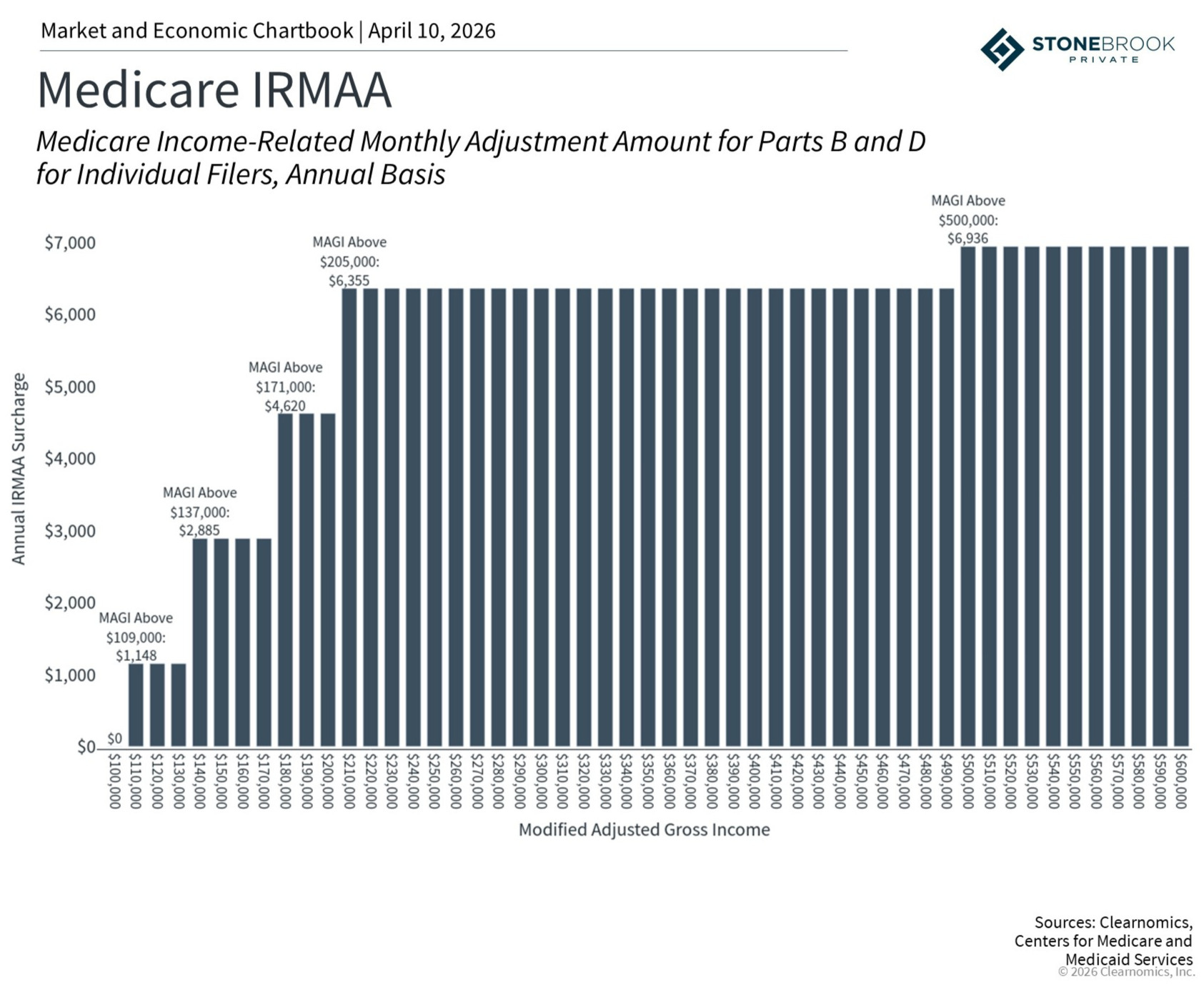

One of the biggest Medicare-related surprises for retirees is IRMAA (the Income-Related Monthly Adjustment Amount). IRMAA is a surcharge added to Part B and Part D premiums when modified adjusted gross income (MAGI) exceeds certain thresholds. For 2026, those thresholds begin at $109,000 for individuals and $218,000 for married couples filing jointly. The amounts are adjusted annually.

Unlike the marginal tax brackets most taxpayers are familiar with, IRMAA operates as a cliff. Exceed a threshold by even one dollar and you pay the full surcharge for the entire bracket. This structure can catch even well-prepared retirees off guard if income edges above a dividing line.

What makes this especially tricky is the two-year lookback: IRMAA is calculated each year based on MAGI from two years prior, since that is the latest tax filing available. A surcharge at age 65, for example, is determined by income in the calendar year the retiree turned 63. Financial decisions made years before Medicare enrollment—Roth conversions, capital-gains realizations, even the timing of Social Security benefits—can all have downstream consequences.

It is also worth noting that IRMAA thresholds and IRS marginal tax brackets are not the same. A common tax-planning strategy is to “fill up” a bracket by recognizing additional income through Roth conversions or similar transactions. However, doing so without considering IRMAA thresholds can inadvertently push a retiree over a cliff, adding hundreds or even thousands of dollars in annual premiums.

Several strategies can help manage IRMAA exposure:

• Qualified Charitable Distributions (QCDs) allow retirees to direct Required Minimum Distributions to charity without increasing adjusted gross income. This differs from standard charitable deductions, which reduce taxes but do not lower MAGI.

• Timing Roth conversions at least two years before Medicare enrollment ensures that the resulting income is reflected in the lookback period before surcharges apply.

• Delaying Social Security can reduce current income and help avoid IRMAA thresholds in the near term, but higher future payments may coincide with Required Minimum Distributions, potentially pushing income above surcharge levels later on.

These trade-offs are exactly why income planning in retirement requires a coordinated, multi-year approach: one that considers tax brackets, Medicare surcharges, and cash-flow needs in tandem.

Medigap vs. Medicare Advantage: a financial planning perspective

Beyond income planning, another consequential decision is choosing between Medigap (Medicare Supplement Insurance) and Medicare Advantage. From a financial planning standpoint, the choice comes down to risk tolerance, lifestyle considerations, and the value a retiree places on predictability.

Medigap complements Original Medicare (Parts A and B) by covering out-of-pocket costs such as deductibles, coinsurance, and copayments. Premiums are higher, ranging from roughly $32 to $550 per month depending on the plan and location, but total healthcare expenses are lower and more predictable. Medigap also provides nationwide coverage, an important consideration for retirees who travel frequently.

Medicare Advantage, by contrast, acts as a comprehensive alternative to Original Medicare. Plans are offered by private insurers and frequently include dental, vision, and hearing benefits. Monthly premiums are often lower, which makes them attractive at first glance. However, they typically carry higher out-of-pocket costs, network restrictions, and referral requirements that can limit access to care. Importantly, switching back to a Medigap plan later may be subject to medical underwriting, which can make the transition difficult or expensive.

Think of the choice in risk-management terms. Medigap offers higher fixed costs with more predictable total expenses, similar to paying a higher insurance premium for broader, more comprehensive coverage. Medicare Advantage offers lower upfront costs but introduces more variability, especially for retirees with chronic conditions or unexpected medical needs. In 2025, the average beneficiary had 42 Medicare Advantage plans to choose from, underscoring the importance of evaluating options carefully each enrollment period.

For retirees with substantial Health Savings Account balances or other dedicated healthcare reserves, the variable costs of Medicare Advantage may be manageable. For those who prioritize budget certainty or who have conditions requiring frequent care, Medigap’s predictability may be worth the higher premium.

Monitoring personal circumstances and policy updates

Medicare planning is not a one-time decision. It requires annual review because available plans, premiums, health status, and income levels can all shift from year to year. Unlike more predictable financial goals, such as education funding, healthcare expenses are inherently variable and tend to increase with age. Ongoing adjustments are an essential part of any retirement plan.

Several additional considerations are worth keeping in mind:

• Timing is critical. Missing the Initial Enrollment Period—a seven-month window centered around one’s 65th birthday—can result in a permanent 10% penalty on Part B premiums for every year delayed, unless the retiree qualifies for a Special Enrollment Period through active employment.

• Medicare provides only limited long-term care coverage. Support is available under specific circumstances, such as a qualifying hospital stay followed by admission to a Medicare-approved skilled nursing facility, but the program is not designed to cover extended custodial care.

• Major life events can trigger a reassessment of IRMAA surcharges. Job loss, divorce, or the death of a spouse may qualify a retiree for an income adjustment, potentially lowering premiums if income has declined.

When navigated well, Medicare can support a more secure and predictable retirement. The key is proactive planning: understanding how the pieces fit together and making decisions with a clear view of the road ahead.

The bottom line? Medicare decisions carry far-reaching implications for retirement income, taxes, and long-term financial health. Understanding the program’s structure, planning proactively around income thresholds like IRMAA, and choosing the right coverage (Medigap or Medicare Advantage) are essential steps to help protect savings and maintain financial stability throughout retirement.

Disclosure:

Stonebrook Private LLC (“Stonebrook”) is a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not constitute an endorsement of Stonebrook by the SEC nor does it indicate that Stonebrook has attained a particular level of skill or ability. This material is provided for educational and informational purposes only and does not constitute investment advice, a recommendation, an offer to buy or sell, or a solicitation of any security, strategy, or investment product. All investing involves risk, including the possible loss of principal. Past performance is not indicative of, and is no guarantee of, future results. Diversification and asset allocation do not ensure a profit or protect against loss in declining markets. Information herein was obtained from various sources believed to be reliable; however, Stonebrook does not guarantee, and accepts no liability for, the accuracy or completeness of information provided by third parties. Charts and data are provided by Clearnomics, Inc. and other third-party providers. Sources may include Standard & Poor’s, LSEG, Bureau of Labor Statistics, and similar providers. Indexes are unmanaged and not investable. Index performance does not reflect the deduction of advisory fees, transaction costs, or other expenses.